CURRENCIES AND GOLD

CURRENCIES AND GOLD

In our econometric model that forms the base of the understanding and

the forecasting of global economy in this website, the currency exchange

rates serve as the grand leading indicators as discussed in Articles

1 , 2

, and 3 posted in

the Section for Everyone. We claim that currency exchange rates lead

the trade balances by roughly two years, and trade balances determine economic

booms and busts in various economic entities acording to their developement

stages and their proprietary domestic conditions, often overwhelming monetary

tools of central banks.

This approach should be contrasted with the main stream approach in

which the galloping globalization accompanied by the exploding trade imbalances

and their determining factor of currency exchange rates are only considered

as none events in shaping the economic booms and busts. This strange attitude

of main stream economic analysts are due to their failure to aknowledge

the importance of trade balance in influencing the evolution of an economic

entity. The often heard ad hoc phrase from those main stream analysts

that the increased amount of total trades (exports plus imports)

boosts economy (but never incorporated into their actual economic analysis)

simply does not stand up to actual detailed scrutiny. For example, during

the boom years of Reagan era, the growth rate of the total trades of USA

is no larger than the mean years of Senior Bush administration; during

the boom years of 1997 to 2000, the growth rate of the total trades of

USA is actually lower than during the preceeding years from 1992

to 1996 with a slower growth rate in the real GDP. It should be emphasized

again that it is the trade balances, not the total amount of trades, that

are shaping the economic booms and busts, and the trade balances are determined

by currency exchange rates. The attempt of this section is thus to try

to extend the leading time of our projections by looking into the future

trends of major currency exchange rates and the price of gold that is closely

related to the relative values of currencies.

General Discussions

Update (Jan. 31, 2007): Yen carry trade and the danger of dynamic hedging

Update (April 13, 2006): From gold to Euro, Yen and Yuan ETF's?

Update (Nov. 12, 2005): Yen carry trade

Discussion: (June 14, 2005)

The trends of Yen/Dollar and Euro/Dollar as discussed in the previous

"Discussion" still hold. The new factor induced in the movement of currency is

the marching-up of US short-term interest rate that is clearly supporting the

dollar (see Comment 17). As has

been pointed out in the comment, the problem arises when the short-term interest

rate hits the ceiling, like 5% in Federal Fund's rate. If the rise of short-term

interest rate stops, dollar will be endangered.

After the last great Dollar buying spree of Japanese Government, Dollar moved

up to 115 Yen/Dollar and subsequently dropped to near 100 Yen/Dollar. If US

Federal Fund's rate marches up above 3.5%, and if there is no sign that Fed will

stop the rate-raising-game at that time, Dollar may test that 115 Yen/Dollar

level. If Federal Fund's rate stops at 3.5%, then we expect the dollar to weaken

vs. yen gradually until enough selling pressure on dollar builds up due to the

persistently large trade surplus of Japan. At that time the resolve of Japanese

government to continue their "weak-yen" policy will be tested again since it may

need to buy up more than 500 billion dollars to assure that yen will be

sufficiently weak to allow Japan to continue to rake in an annual trade surplus

near 200 billion dollars.

As US stock prices continue to stagnate, the income of Wall Street may have

peaked. This will be negative to the export of European made luxury goods. Thus

the trade surplus of Europe vs. America may have peaked too. In conjunction with

the disarray and the popular discontent with pan-Europe movement and Euro within

Europe, we may see persistent weakness of Euro as a whole. Though the habit of

currency traders to link Euro with Yen is not easy to nullify and Euro will

still go up and down vs. Dollar as Yen moves up and down vs. Dollar, we will see

that the rate of Yen/Euro moves persistently against Euro. Up to now Euro buyers

are more or less identical to gold buyers. However, as Euro loses the market

favor, those buyers probably will just turn to gold and the link between gold

and Euro will be broken.

The dark horse in the currency game is Chinese Yuan. As depicted in

Comment 15 and

Article 6, pressures from both the economic

and the political fronts are mounting to push Yuan valuation higher. There are

several possible scenarios about the fate of Yuan, each with slightly different

outcomes. To peg Yuan to a basket of currencies instead of to Dollar may not be

a good solution. Suppose Yuan is pegged to Dollar, Yen and Euro with equal

weights. Yuan may even devaluate against Dollar if Yen and Euro fall against

Dollar. If Yuan is just upward revaluated against Dollar, then the question is

what is going to happen with Yen and Euro. We believe that the condition to push

Yen and Euro before the revaluation of Yuan will still operate and Yen and Euro

probably will continue their own courses. The worst case is that China refuses

to revaluate Yuan, and US congress imposes punitive import tariffs against

Chinese made goods. The consequences of such a case is already discussed in

Comment 15 so they will not be repeated here.

Discussion (January 19, 2005)

From now on separate discussions about Yen and Euro will not be updated

and the category of gold will not be launched, since this general discussion

section is actually about US Dollar and naturally cover all those other

currencies and gold.

For the general direction of Dollar, readers are urged to read the January

17, 2005 discussion of US economy in the projections sector. Japanese Yen still

has hard time to break the 100 Yen/Dollar barrier. The main reason of this

hesitance is the 300 billion plus dollar-buying operation done by

Japanese Government from the mid 2003 to the spring of 2004; that huge dollar

buying frenzy has temporarily absorbed the selling pressure of dollar. It will

take time for the selling pressure on dollar to rebuild as US trade deficits

accumulate month-by-month. Under the weak selling presuure environment that

is artificially created by Japanese Government, the currency market is

hesitant to challenge that 100 Yen/Dollar line since Japanese Government is

certain to come into market to defend it and will succeed with a rather modest

amount of dollar buying. Market always fluctuates. When it is not going to

challenge that 100 Yen/Dollar line, then Yen will retreat. That is what happened

when Yen retreated to near 105 Yen/Dollar level. For the time being Yen will

probably fluctuate between 100 Yen/Dollar and 105 Yen/Dollar, waiting for the

selling pressure on Dollar to reaccumulate. Only then Yen will challenge 100 Yen/Dollar

barrier with a decisive force, and force Japnese Government to conduct a

one trillion plus dollar buying operation or else. Of course, anyone who wishes

a stable global economy will be loath to see what happens if this else-senario

developes.

Euro is overpriced compared to Yen. Europe is the major exporter of luxury goods

ragning from luxury consumer goods, gourmet foods, and high priced mechanical

devices. The luxury good buyers, ranging from the group enriched by the windfall

from the high oil price to the ones bestowed with bonuses generated from the

windfall of managing the enormous imbalance in the global economy. Those affluent

buyers certainly will not be detered by some slight price appreciation of European

goods due to the high flying Euro. Thus the favorable trade balance of Europe will

continue and that in turn becomes a strong support of Euro against US Dollar.

The movement of Euro is synchronized with Yen. However, with Yen capped by

100 Yen/Dollar line, the market pressure for a weaker Dollar is disproportionally

shifted to Euro, since the market conception is that European Central Bank only

barks but does not actually bite. As Yen fluctuates between 100 Yen/Dollar

and 105 Yen/Dollar, Euro will follow Yen but with an amplified movements.

Only when Yen breaks that 100 Yen/Dollar line and Dollar starts to enter a

free-fall phase versus Yen, then Euro will lag behind Yen in its rate of

appreciation against Dollar.

Gold is used as the currency hedge against Dollar. It is especially synchronized

with Euro. This is becuase Japanese are less fond of gold than Europeans and

people in other areas. For US residents gold is also a strong hedge against

the devaluation of Dollar since it is extremely difficult for US individuals

to invest in non-US currencies as a long term investment.

Questions about Chinese Yuan: (Nov. 21, 2004)

The question whether Chinese Yuan will revaluate upward or not has become

a hot topic in the economics and financial circles recently. It is a good

time to have a comprehensive view of China situation and to study what

kind of effects of Yuan revaluation will have on global economy. As emphasized

in various places throughout this website, and particulary in article No.4,

if a high wage economic entity like Japan and Taiwan artificially depress

the value of their currency through currency market manipulation, just

as they are constantly doing, their trade surplus will be artificially

inflated and their comsumption power will be transfered to the trade deficit

country, resulting in the long lasting economic booms in the trade deficit

country and chronical recession in the trade surplus regions like Japan

and Taiwan. However, the situation in China is very different from Japan

and Taiwan. China has a large pool of under utilized labor resource, and

an investment friendly environment like lax environmental control, little

labor discord and stable political environment; it is natural that international

capitals are drawn to China like a torrent and is rapidly transforming

China into the factory of the world. When $100 worth of goods is produced

in China, $90 worth of it will be exported to USA to be spent by Americans,

but still $10 will be retained by China. It should be noted that it is

Japan and Taiwan that are paying out this $100 from their pocket, but not

from the pocket of China. Thus this set up enriches China, make American

economy boom, and make Japan and Taiwan in chronically poor economic situation.

If Chinese just save the $10 from their production of $100 worth of goods,

then China will also contribute to the enrichment of American consumer

but do litle to improve its own living condition. In the current situation

Chinese are more than happy to spend the money dropped by Japanese and

Taiwanese merchants, and as the result the overall trade surplus of China

is substantially less than that of Japan and even less than the tiny Taiwan

despite its enormous trade surplus with USA. Under such an environment

if Chinese Yuan is upwardly revaluated against US Dollar, whether the production

cost in China will rise accordingly or not is determined by the labor force

availability and how flexible is the wage determination process in China.

If Chinese labor market is still in the condition of more supply than demand,

then when Yuan is revaluated Chinese wage in terms of Yuan will simply

drop and Chinese wage in terms of Dollar will stay more or less the same;

thus the revaluation of Yuan will not raise the production cost in China.

If Chinese labor market is already tight and the pressure for higher wages

is already on, then the revaluation of Yuan may simply ease the pressure

on wages; in this case the revaluation of Yuan also will not affect the

rising production cost in China. Only if Chinese wages are inflexibly fixed

by some external force to a certain amount in Yuan, then the upward revaluation

of Yuan will push up the production cost in China and reduce the attractiveness

of China as the heaven of international investments. We doubt very much

that the last senario is the reality, thus we do not expect that the upward

revaluation of Yuan will do any long term alternation of the global economic

situation. There is some sign that Chinese labor market is getting tight

and the pressure of wage inflation may appear soon. Thus no matter whether

Chinese Yuan is revaluated or not, the cost of production in China will

rise soon and multinational capitals will start to look for other cheap

labor sources for their production facilities. If China insists on to retain

its vast export industry even its production cost is rising steadily through

the currency market intervention like Japan and Taiwan are doing, then

China will also push away its own saving pool toward USA for America consumer

to spend whereas Chinese consumer will suffer the same fate as their counter

part in Japan and Taiwan.

The Danger of a Currency War : (Sept. 28, 2004)

Right after the warning about the danger of a hasty dollar devaluation

in this space, news has come in to let us worry about the eruption

of a currency war that will lead to a substantial devaluation of dollar

and the destruction of the current order of the globalization. This time

the danger is not coming from some unnamed US high officials as the case

of the previous warning, but come from China. In an editorial on China

Daily (the official English language newspaper of China) the diversification

of Chinese Government's vast and dominantly dollar denominated foreign

currency holding away from Dollar but into Yen and Euro is urged in order

to avoid the unavoidable collapse of US Dollar. If China is going to sell

a significant portion of its dollar holding for Yen, say 200 billion dollars,

then Japan must immediately buy those dollars by selling yens, otherwise

Dollar will collapse immediately against Yen and the previously mentioned

danger of a hasty devaluation of Dollar becomes reality. The same thing

will happen if China sells its dollars for Euro. The fact that China holds

enormous amount of dollars is the result of its policy to peg its currency,

Yuan, to Dollar at a fixed rate so that China can maintain its low labor

cost advantage, attract vast amount of capitals from Japan and Taiwan (US

is a capital importer, all the investments of US corporations into China

are nothing more than the recycling of capital borrowed from Japan and

Taiwan), manufacture goods and export them to US, a major link for US to

run up such a trade deficit. In pursuing this kind of policy, the sure-to-come

dollar-collapse risk is what China should have known and must shoulder.

If Japan is forced to shoulder the burden of holding dollars alone, then

very soon Japan will be forced to buy up one trillion dollars or more within

a year, a political suicide even for almighty Japanese financial bureaucrats.

If Japan let Yen (and Europe let Euro) rise because of China's dollar selling,

whereas Chinaese Yuan continues to be pegged to Dollar, then Chinese goods

will flood Japanese and European markets. With US imports from Japan and

Europe plumetting due to the collapsing dollar against those currencies

(thanks to China's dollar selling), both Japan and Europe must turn their

huge trade surpluses into huge trade deficits, with China continuing to

racking up huge capital inflow and exclusive position as the suppliers

of manufactured goods to the whole world. Certainly Japan and Europe

are not like US that has wantonly used run away trade deficits to temporarily

boost US consumption by sacrificing the future financial health of the

country. We must note an under reported recent incidents in Spain; a group

of out of job shoe factory workers resorted to terroist-like tactic to

attack a Chinese shoe distributer and burned down truck loads of made-in-China

shoes. We can expect that the whole order of globalization will crumble

down quickly and a depression will hit the whole world, including China,

if Dollar collapses suddenly due to the diversification of dollar holding

by Chinese Government.

A more unthinkable but highly likely senario in case China starts to

diversify a nonnegligible amount of its vast dollar holding into Yen and

Euro is for Japanese Government, or Euro Central Bank, to announce its

desire to diversify a certain portion of its even larger dollar holding

into Chinese Yuan. Though it is not easy to buy vast amount of Yuan on

an open market, hot money will do the trick for Japanese Government in

that occasion. Chinese Yuan will feel an enormous pressure to upward revaluate,

and Chinese Government will end up buying more dollars to keep Yuan pegged

to Dollar than the dollars it wants to diversify! The consquence of such

an outright currency war between China and Japan, and possibly between

China and Europe will lead to an outright collapse of Dollar and a certain

world wide depression since during such a currency war both sides want

to sell Dollar for something else.

Ironically there is a safe thing that China can diversify into. That

is gold. However, the world wide gold market is thin. If China wants to

convert several hundred billion US dollars into gold, the price of gold

will skyrocket to the delight of gold bugs. When China finishes with the

gold buying, then the price of gold will fall back, causing China heavy

capital loss. But the venture into gold by China will not disrupt the balance

on currencies and will have a minimum effect on the globalization scheme.

The Danger of Hasty Dollar Devaluation : (Sept.

26, 2004)

A UK press report says that some high officials within US Government

are pressuring The Treasury Department and the White House to bring up

the issue of a 20% devaluation of US Dollar against major trading currencies

in the upcoming G7 meeting. The reason quoted is the worry of the run away

trade deficit of US and the danger it poses to the world economy. At a

time so close to the general election of USA, and the issue of job outsourcing

seems increasingly to become a serious election issue, this test baloon

may well be an attempt to deflect the possible attack from the opposition

on that issue, and is launched from those care more about the election

than the real economy. The imbalance in trades is not a sudden problem

of today; it has been created by the globalization the flood gate of which

has been opened by Reagan administration and the problem emensly intensified

during Clinton adminstration. As explained in articles posted on this website,

this run away trade deficit is the back bone of the globalization. Though

it poses as an enormous threat in future, up to the present it is really

the underpining reason of Reagan era and Clinton era prosperities of USA,

the reason of rapid growth of China, India and other tigers of Asia, but

is a bane on Japanese economy. A sudden and hasty devaluation of Dollar

will throw this whole globalization structure into chaos and will certainly

create a world wide sever economic downturn within two to three years.

Running a trade deficit is equivalent to borrow from foreigners. At

the time when US consumers save almost near zero amount of their income,

the borrowing in the form of trade deficit, amount to 600 billion dollars

a year, becomes the major pool of funds available for US residential, corporate

and government borrowers. An attempt, like this proposal of 20% devaluation

of Dollar, to curb US trade deficit will immediately endanger this essential

source of funds for all kinds of US borrowers, and will push US economy

into another sharp and painful recession within two to three years. Let

us recall the history of Dollar devaluations and their consquences. The

1985 devaluation of Dollar against Yen preceeded two to three years of

the turn of US trade deficit in the late 1987, acompanied by a sudden collapse

of the stock markets and an eventual economic down turn that only bottomed

out at the end of 1991. The twin devaluations of Dollar in the summers

of 1998 and 1999 were the precursor of the burst of the US bubble starting

at the end of 2000. The twin moderate drops of the value of Dollar in the

spring of 2002 and 2003 are now causing the moderate slow down of US growth

rate until the end of 2005. A 20% devalaution of Dollar now will cause

US trade deficit to be curbed around the latter half of 2006 and an economic

recession in the latter half of 2006 to 2007. As the US trade deficit wanes,

export based economies of China, India, other small Asian countries, Mexico

and other Latin America countries will all feel the pinch. That adverse

effect will propagate to resource exporters like Canada, Australia, Russia

and South Africa, and thus a global recession will be ensured. The currencies

of those export depending countries will then slump against Dollar, the

devaluation effect of Dollar will be graduately wiped out, and US trade

deficit will resume its growth unless the barriers to free trades are reelected.

Europe will continue its near zero growth rate and high unemployment rate

course; its economy is just too stoggy and inflexible to be quickly influenced

by those economic dynamics like a sudden change of the value of currencies.

Ironically it will be Japan that may benefit from the devaluation of Dollar.

Japan will be saved from the misery created by its own financial planners,

that is, the endless manipulation of the currency market to keep Yen weak

and Dollar strong. As Japan's trade surplus diminishes, large amount of

funds can remain in Japan to fuel its consumer spending and fixed assest

investment to pave the road to a new boom, in stead of lending those funds

to US and let Americans spend them as in the current situation.

The current imbalance in the trades is created by ill advised government

manipulations in the currency markets. What the world economy needs is

not more secret deels in G7, but a pledge by all governments to keep their

hands off currency markets and let the market take care of the imbalance.

Huge market volatilities are not caused by currency speculators as manipulation

happy government officials claim, but is caused by the desire of those

officials to distort the values of their currencies to run trade surpluses

on one hand and market participants, including speculators, trying to fight

those evil manipulations on the other hand. If government officials withdraw

from the markets completely, it will be the left hand of speculators fighting

the right hand of speculators, and speculators will abandon currency market

since there is no big counter part, the governments, and there will be

no big gains. A truely free currency market has a natural policing mechanism

to counter the artificial means to increase trade imbalances. If all the

governments keep their hands off curreency markets now, Dollar will fall

gradually. US trade deficit will peak and then start a gradual decline

as the percentage of GDP. Deprived of the artificial means to use trade

deficit to boost consumption, and deprived of the disinflational effect

of huge trade deficits, US economy will enter a prolonged stagflation period.

However, during that painful rehabiliation period, first US job outflow

will slow down, and then US manufacturing sector will rebuild gradually.

Only then US economy will regain its health and becomes capable of a new

era of balanced growth. As for "export is the king" Pacific rim countries,

they will loose means of quick rich through importing capitals from

Japan and Taiwan, and export manufactured goods to USA, but needs to painstakenly

clean up their own domestic social structures to create an environment

capable of self-reliant balanced growth, or else they will stay as under

developed countries forever.

This UK report is already creating a sudden move in the currency market.

How bond and stock markets will react when markets open tommorow is anyone's

guesss. Recently The Secretary of Treasury reiterated the pledge of "strong

Dollar" policy, a catch phrase has not been heard for a while. Now looking

back, that reiteration probably underscores the reliability of this UK

report, as the common saying goes, "there will be no smoke if there is

no fire."

Divergence of long and short term interest rates in USA and its implication

to currency markets: (Sept. 23, 2004)

In recent months Federal Reserve Board is steadily raising short term

interest rates with the rehtoric that US economy has regained "traction"

and is going to boom, thus the rise of interest rates is necessary to prevent

the economic overheating. On the other hand the 10 year Treasury rate peaked

at 4.8% some time ago and is steadily falling, now below 4.0% again. The

rehtoric of the falling long term interest rates is based on the market

expectation that US economic growth is going to slow down, and there is

little danger of overheating. Some market participants are raising the

question who is right, Mr. Greenspan or the market? Before we answer

that question, we should note that US Federal Reserve Board under the rein

of Mr. Greenspan is prudent and cautious, not like Japanese monetary authority

that is famous for its monetary policy to swing from one extreme to another

extreme. If the concern of overheating economy is the real reason behind

the rise of short term interest rates, then Federal Reserve Board has ample

time to sit back for a few months after the initial two 0.25 point raises,

make sure about the economy's performance for a quarter or so and then

decide what to do next. The insistence of Federal Reserve Board that it

must raise interest rates in a steady pace certainly does not match with

the genuine anxciety about the overheating of the economy. Then what is

the unspoken reason behind this insistence of the rise of short term interest

rates? We interprete that the reason is the worry about the value of US

Dollar. Japanese Government has bought more than 400 billion dollars during

a nine month period recently, and has temeprarily absorbed all the selling

pressures on US Dollar. However, as the run away US trade deficits continues,

it is just a matter of time that enormous selling pressure on US Dollar

will return. During the last Dollar buying frenzy of Japanese Government,

discords has appeared already within Japan questioning the motive of this

fanatic Dollar buying activity, though the discord has appeard in a very

strange and unexpected way (see Article No. 8 posted in this website for

that event). If the huge Dollar selling pressure reemerges soon, it will

be questionable whether Japanese Government can pursuade Japanese people

that it should buy like one trillion dollars to prevent the collapse of

US Dollar. Contrary to their official attitude, Federal Reserve Board knows

well what a collapsing Dollar will mean to US economy. We may say that

recent movement of the currency market indicates that Japanese Government

does not have the ability nor the desire to push Dollar much higher above

110 Yen/Dollar. Dollar is holding on to that level simply because the declaration

of Fed. to raise interest rates steadily. Thus Federal Reserve Board simply

can not afford not to raise interest rates and take the chance of a suddenly

collapsing Dollar that requires again an emergency rescue by Japanese Government

that it may not be able to deliver. Based on this line of reasoning, we

must expect that the rise of short term interest rates will continue in

spite of the slowing GDP growth rate in near futre. As the short term rate

rises, the long term rate will stop falling since very soon the carry trade

(borrow short term and buy long term debt instruments) will stop to make

any sense.

Euro/US Dollar

Discussion (Nov. 21, 2004):

In spite of the steady rise of Euro vs. US Dollar the trend of which

has started in the spring of 2002, and inspite of the general two-year-delay

effect of currency movement on the actual trade balance, Euro region's

trade surplus has not shown meaningful decline yet, although its growth

rate probably has slowed down quite a bit. That is the reason that Euro

is still rising and causing wild speculations in the Euro-Dollar market.

However, the rise of Euro has gradually gathered steam from the latter

half of 2002 and into 2003, and its trade-surplus-supression effect is

still to be earnestly felt. It is when Euro region's trade surplus starts

to shrink then the rise of Euro vs. Dollar will come to an end; such a

day may not be far away.

Discussion (Aug. 3, 2004):

According to Euro stat, the trade surplus of euro region peaked in March

of 2004, and the surplus has declined consecutively in April and May of

2004. We are just witnessing the very first effect of strong Euro that

spans from the spring of 2002 to the spring of 2004. As the effect of strong

Euro steadily been felt, the trade surplus of Euro region will continue

its long slide; the slide has another one year and ten months to go. Under

this kind of shrinking trade surplus environment, Euro will weaken further

against Dollar.

Discussion (May 15, 2004):

The shape of the global economy, especially the economy of USA, is heavily

influenced by the cross Pacific Oscean trade imbalance, not by the cross

Atlantic Osean trade balances. If USA, Asian Pacific Rim region, and Europe

are portrayed as three economic giants, USA and Asian Pacific Rim are embraced

in a dance toward the catastrophic trade imbalance whereas Europe just

stands at the side line watching. In that sense the exchange rate of Euro/US

Dollar does not come in as a prominent factor in projecting the shape of

global economy, though the rate apparently determines the trade balances

of Euro region. It should be pointed out that due to the socialistic and

stoggy economic strucutres of Europe, the effects of trade balances on

European economy is much more muted than to robust and flexible economic

entities like USA and Asian Pacific rim countries. However, due to the

absence of currency market manipulation by European Central Bank, the movements

of Euro vs. US Dollar can be understood by pure logical considerations

based on the economic environments and political events as depicted in

Article 3 posted in the

"Section for Everyone". This means that we can project the future trend

of Euro/Dollar with much more certainty than the all important rate of

Yen/Dollar.

Steadily weaker Euro vs. US Dollar since the inauguration of Euro in

1999 has boosted the trade surplus of Euro region against USA. Especially

the sharp escalation of Euro region's trade surplus starting at the first

quarter of 2002 signaled to the currency market that the weakness of Euro

was overdone. Thus Euro has staged a turn around and strengthened against

US Dollar up to the spring of 2004. Now the effect of the turn around of

Euro in the spring of 2002 is coming in and the trade surplus of Euro region

is eroding fast. As the trade surplus of Euro region evaporates the period

of strong Euro is also ending, and we expect that Euro will slide down

against US Dollar until the spring of 2006 whereas the trade surplus of

Euro region will erode steadily and finally turn into a trade deficit.

Japanese Yen/ US Dollar

Discussion (Nov. 21, 2004):

As repeatedly emphasized by us Japanese Yen is artificially supressed

vs. US Dollar by the currency market manipulation of Japanese Government,

and the long term trend is to push Yen substantially higher (probably to

above 80 Yen/Dollar level) in order to dent the enormous trade surplus

of Japan and reduce the impossible to sustain US trade deficit to some

degree.The lull in Yen-Dollar market since the spring of this year is simply

due to the enormous intervention of Japanese Government in the preceeding

period and has temporarily absorbed a large part of the selling pressure

on Dollar. Now the market is testing the nerve of Japanese Government again;

it has pushed down Dollar through 110 Yen/Dollar level without reigniting

the market intervention of Japanese Government; it has pushed Dollar down

through 105 Yen/Dollar level and still Japanese Government has not come

into the market yet. It is now testing 100 Yen/Dollar level to see whether

or not Japanese Government will put money into where its mouth is and come

into the market. If Dollar breaks the psychologically important 100 Yen/Dollar

level, Dollar can quickly sink to 90 Yen/Dollar and even to challenge the

all time record of 80 Yen/Dollar. If that senario happenes, then Japanese

Government will need to spend another enormous sum of Yen in order to reverse

that trend, whereas if it comes into market before Dollar breaks 100 Yen/Dollar

line, much smaller amount of market intervention will do the trick.

Discussion (Aug. 3, 2004):

The near ten month massive currency market manipulation of Japanese

Government has mopped up around 400 billion dollars from the market. It

has temporarily absorbed all the dollar selling pressures, and is allowing

Dollar to float freely without much danger of severe drop in its value

against Yen. It will take a while for the dollar selling pressure to rebuild

as US current account deficit accumulates and more and more Dollar get

into the hands of foreigners. Only when enough dollar selling pressure

rebuilds, it is a question of when but not whether, the resolve of Japanese

Government to artificially depress the value of Yen will be retested with

enormous firework.

Discussion (May 18, 2004):

The driving force of the global economy, that is, the cross-Pacific

Oscean trade imbalance is driven by the artificially supressed Asian currencies

vs. US Dollar. The most important currency exchange rate is Yen/Dollar

rate. We should not just look at the trade balance of each individual country

with USA, but need to look at the total trade surplus of each Asian country.

For example, the total trade surplus of Japan is reported as around 120

billion dollars a year whereas China's total trade surplus is only around

30 billion dollars a year, though the direct trade surplus of China with

USA far exceeds that of Japan. This is because there are many proxy exporter

countries for Japan; Japan exports components and manufacturing know-hows

to those proxy exporters, produce goods in those countries and for those

countries to directly export to USA. Furthermore, if we look at the world

trade statistics of WTO, every year the total amount of imports of the

whole world always exceeds the total amount of exports of the whole world

by a few hundred billion dollars. This implies that there is a systematic

trend for countries to under report exports and over report imports. If

we look at the trade statistics of Japan, there is a category called "error

and omission" the amount of which can be as large as the trade surplus

itself. There is a reasonable doubt that the actual trade surplus of Japan

may be substantially larger than the officially reported number.

The currency exchange rates are determined by the demand and the supply

on various currencies. There is no such thing as the proper exchange rates

reflecting the proper economic conditions; that is only the excuse of governments

to intervene in the currency market and distort the selfregulating global

economy. In a currency market free from any government intervention the

free market will not allow any country to run trade balance at one direction

for a long time. Suppose USA is running a trade deficit. US dollars are

handed to foreign exporters. Since US Dollar is not the legal tender at

foreign countries, those received dollars must sell them to recoup their

production costs and profits so that selling pressure of US Dollar mounts.

Then the value of dollar will go down vs. other currencies, the production

costs of other countries rise, and the trade deficit of USA will be wiped

out. Thus in order for other countries to continue to export and run trade

surplus against USA, their governments must intervene in the currency market

to prevent the fall of US Dollar. Those governments know well where the

production costs of their exporters are, and the so called "proper exchange

rate level according to the economic condition" is actually the level of

exchange rates where their exporters can continue to export to USA, not

the true proper exchange rate level between two currencies that only a

truely free currency market can determine.

Since 1993 the exchange rate of Yen/Dollar has been the tug of war between

the market force and Japanese Government. The market force wants Dollar

to go down and Yen up so that the run away USA trade deficit and the large

trade surplus of Japan can be corrected and the global economy can be returned

to a balanced and sound footing, whereas Japanese Government wants Yen

to be kept weak against Dollar so that Japan can continue to run large

trade surplus and USA hooked on the habit of "borrow and spend" due to

the run away trade deficit, even at the risk that such a practice will

push the global economy into a catastrophic imbalanced condition and will

eventually collapse in the form of a worldwide depression. In the following

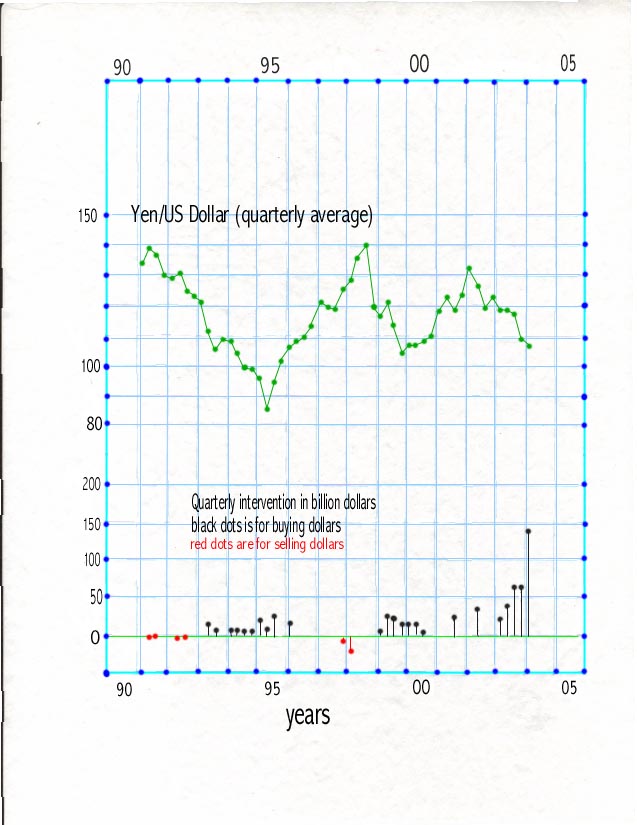

figure the currency market intervention of Japanese Government since 1991

is graphed.

The green dots are the quarterly average of Yen/Dollar rate, the black

dots with a black vertical line are the quarterly sum of net dollar buying

by Japanese Government in units of billion dollars, and the red circle

with a red vertical line are quarterly sum of net dollar selling by Japanese

Government. When the Yen/Dollar rate falls from the peak of 1991 and dip

below 110 level at the second quarter of 1993, Japanese Government started

to intervene by buying up dollars. This first round of dollar buying operation

continued until the first quarter of 1996 (totally bought 110 billion dollars).

This massive dollar buying had absorbed all the dollar selling pressure

at that time and more, and consquently had sent Dollar sharply higher toward

its 1998 peak. This deliberate pushup of Dollar had triggered Asian economic

crisis (see Article 1 posted in

the Section for Everyone), and

the panicked coordinated dollar selling intervention to cool down the

Yen/Dollar rate in the final quarter of 1997 and the first quarter of 1998(

but to no avail). During that period the trade deficit of USA has been

accumulated steadily and the potential dollar selling pressure had been

building up just waiting for some trigger to erupt. The trigger came in

the form of Russian currency crisis in the summer of 1998 and a near miss

of the collapse of the world financial system, and the erupting dollar

selling pressure had sent Yen/Dollar rate shaply lower. The Japanese Government

restarted to buy up dollar anew in 1999, continued for 5 quarters to absorb

all the dollar selling pressure at that time, and dollar started to move

higher again. The third quarter of 2001 intervention is due to the attempt

to boost dollar at the time of 911 tragedy and had finally sent Yen/Dollar

rate to its peak of 2002. This second round of intervention consisted totally

of buying 123 billion dollars. Probably this second round of dollar buying

intervention was not forceful enough, so dollar selling pressure has build

up quickly and Yen/Dollar rate has started to plunge again in the spring

of 2002, triggering the third round of dollar buying operations of Japanese

Government. Up to now Japanese Government has already bought 360 billion

dollars in this third round of intervention, and apparently has absorbed

all the dollar selling pressure at this moment. That is why Yen/Dollar

rate is moving up again starting from April, 2004 and is approaching 115

level. A retracement to 110 level will come, and will test Japanese Government's

resolve to defend the weak Yen policy. If Japanese Government come in with

a forceful intervention, then Yen/Dollar rate can be sent above 115; actually

Japanese Government can push the rate up to whatever level it wants at

this moment if it is willing to buy a few hundred billion dollars more.

If Japanese Government only intervenes moderately then the Yen/Dollar rate

can be hoovering around in the band of 110 to 115 for a while, but the

dollar selling pressure builds up due to the continuously accumulating

huge US trade deficit, waiting for the next round of Dollar weakness to

be triggered. If Japanese Government does not intervene when the rate retraces

to 110, then it will fall below 110 and start to test the resolve of Japanese

Government anew at 105 level and so on. If Japanese Government has already

given up on currency market manipulation, then the rate will fall sharply

to whatever level necessary to wipe out the huge trade deficit of USA;

in that event US economy will fall into a severe recession in 2006 to 2007,

and Asian export industries will also receive a severe blow. We do not

believe that Japanese Government has the determination of this rough treatment

to correct its own mistake of artificially manipulating the Yen-Dollar

market, so some kind of intervention can be expected to continue as far

as the eye can see and the global economy will be pushed gradually toward

the ridiculous picture as depicted in Article 7

in the Section for Everyone.